Advice from the gardening column: XP Power edition

I have a friend - a journalist - who refers to the stock-tipping parts of his newspaper as "the gardening column": full of plants he says.

But the Financial Times is not any ordinary newspaper - and its stock tipping columns should be a little better than that. So I read David Schwartz column on how to manage your investments on holiday with great interest. Fantastic stocks - ones you can put in the bottom drawer and know they will deliver - they are the stuff I need to take the stress out of my life.

Here is what he recommends:

Turning to my own portfolio, I have just bought shares in XP Power (XPP), a designer and manufacturer of power converters. These are devices that allow electronic equipment to operate efficiently.

XP Power shares were in the 1,600-2,000p range during the first half of 2011. But investors ran for cover after the level of new orders began to slip in mid-year. The slowdown eventually caused lower profits in the first half of 2012.

But the company’s order rate is now spiking higher. I expect second-half results to be much higher than last year’s figures.

Even better, XP Power is quite optimistic about its future. It recently launched 10 product lines. It brags about its strong design win record in the current year. The share of revenues derived from products manufactured internally is rising. These are more profitable than those manufactured externally. Its new factory in Vietnam has just come on stream, which will also help to increase margins.

The dividend has just increased and now approaches 5 per cent.

Power converters - the things you plug into your laptop or into the life-sign monitoring equipment in a hospital to feed them nice stable DC current - don't seem to me to be a massively prospective business. There are lots of suppliers. I am not particularly fussed about which one I use. If I want power reliability then I get an "uninterruptable power supply" and even those are a competitive market. I would expect a story of thin margins made good only by lots of product development and fairly large sales.

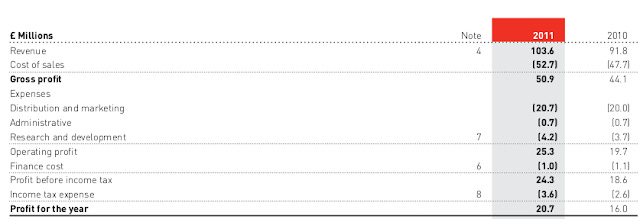

XP Power confounded my expectations. Completely confounded them. The accounts were nothing like what I expected to see. Here is the P&L from the last annual report:

Revenue was £103.6 million. Gross profit was £50.9 million. The gross margin was 49.1 percent.

Operating profit was £25.3 million. Operating profit margin was 24.4 percent.

Research and development expenditure of a mere £4.2 million pounds. Not a big number - but a moderately healthy 4.1 percent of revenue.

These ratios looked strangely familiar. But I could not quite put my finger on why. And then a light went off in my brain. A light from Cuppertino. Apple! Yes that company.

Here - and on an entirely different scale - is Apple's P&L for the last three years:

The sales last year were $108.2 billion. Gross margin was 43.8 billion. Gross margin was 40.5 percent - a little lower than our humble XP Power. But Apple's operating margin (31.1 percent) is higher than XP Power.

But hey - David Schwarz - writing for the esteemed Financial Times - tells us that XP Power is going to increase its margins. Apple like numbers here we come!

XP Power history

By now I am seriously impressed with XP Power. It makes a seeming commodity electronic product but has a higher gross margin than Apple. Surprisingly despite the fact that it does not advertise much or run all those fancy stores it manages - after SG&A to wind up marginally - and only marginally less profitable than Apple.

Pretty darn impressive.

If it just turned up this way - a new entrant into the realm of super-profitable electronic hardware companies - then I would be surprised - but not stunned. But XP Power has been pushing out astounding numbers for a decade. Larry Tracey - Executive Chairman - is quoted in the last annual report as follows:

Our strategy and its execution resulted in earnings per share of 106.4p for 2011, an increase of 27% over 2010. The compound average growth rate of earnings per share has been 27% over the last 5 years and 18% over the last 10 years.

It is not Apple - but this is way more impressive than most companies. 18 percent for 10 years is more than 500 percent growth. Previous years are also at very high margins.

Wow. Now I am really wondering why it took a share-tipping column to alert me to this wonder stock.

XP Power products

By this stage I had found a nearly unknown electronics company with margins nearly the match of Apple and with a hugely impressive growth rate. And it did what looked to me like a commodity business.

I had to go looking for their products.

Alas they were harder to Google than you would think - if only because XP Power got mixed up in articles about the Microsoft XP operating system and computer power requirements. Here however is a typical example:

It is a simple 15 watt DC converter (about a quarter of the capacity of the converter for my laptop). It is priced at 28 quid - cheaper in quantity. Still this is more expensive than the cheapest laptop computer DC converters suggesting that higher than normal margins are possible.

The balance sheet puzzle

An electronics company with a proud history (rapid, continuous growth) and margins within a whisker of Apple would normally - I expect - have a balance sheet similar to Apple. Maybe not in size - but I would expect to see a lot of cash - cash being the tangible representation of past profits.

But XP Power does not look like that at all. Here is the balance sheet:

The balance sheet has on it lots of assets representing past profits. Notably it has 31 million pounds of goodwill (they have purchased very well as acquisitions have not diluted profits). They also have 22 million pounds in inventory.

But they have that very un-Apple like thing. Net debt. Strange given their profitability - but with this record - well - you just have to trust them.

But I will not be buying the stock

David Schwartz "holiday buying case" for XP Power is that it will have increasing profitability. That is for a company that is already trading with Apple-like margins.

I am an old fashioned kind of investor. I like to think what a company will look like in five years before I pull the trigger.

To buy this stock I would need to be able to finish the following statement: I believe XP Power will in five years time have margins similar to Apple because...

I can't answer that. Indeed I can't imagine that you can stay this profitable in a seeming commodity business - so I shorted the stock. Maybe I need to find another gardening column.

John

To clear up confusion with my North American readers who forget there is a stock market in Old Blighty - this stock trades in London measured in pounds. [The Americans who forget there is a world outside the lower 48 know who they are!]