Brambles - some thoughts

After twenty five years of disappointments is it time?

It is pretty rare on this blog that I write up a long case. And I have never written one up on a company whose origin is my home country (Australia).

But I wrote this for my last client letter and it was edited out for length. As per usual I want comment and expect people to disagree with me.

Also note that I am putting this up even though it was written originally a couple of months ago. Since then there has been a slight miss on revenue - but the company reaffirmed on guidance. The stock did not like that - because - well - as you will see - this company is one that never fails to disappoint.

===

Brambles

Necessary clarification. Brambles is a June 30 balance date company. When we say something happened in 2016 it happened in the 2016 financial year that runs from 1 July 2015.

Not every stock we write up we love. We wrote up Hibbett in the December letter and we loved that position. Alas it got taken from us in a takeover we regard as underpriced.

In this letter we will write up an Australian but global business (Brambles) business which we think is okay rather than special. If things go well, it could work very well. The company has excellent financials but a distinctly patchy history. The patchy history means that (relative to other companies with similarly excellent financials) it trades a discount.

The question with this one is whether the patchy history is prologue. We do not think it is and indeed we finish with a suggestion that should ensure the future is different from the past.

We own this stock because we believe the current business model (and the current numbers and the seeming prospects) is different from the past, and the company no longer deserves the discount it trades at.

The write-up here is really an attempt explain the patchy history but also detail why it is not prologue. As the patchy history is the issue this note goes into considerable historical detail.

The write-up should also be read in conjunction with our previous quarterly letter which showed some businesses that had excellent economics (witnessed by high returns on assets (ROAs) and returns on equity (ROEs). Some of these businesses we thought might be sustainably excellent. Others – as per the last quarterly letter – were utterly awful.

We are not entirely sure where to put Brambles.

Brambles – an okay business

At the back of every Walmart and most consumer retail stores you will see a stack of humble pallets – the pallets that go from (say) the razor blade supplier to the Walmart warehouse and from the warehouse onto the retail store.

Most of these pallets will be painted blue. Some will be red. Some will have no paint at all. The blue and red ones will generally be better made because they are recycled. Someone picks them up and delivers them elsewhere and fees are paid. Those pallets will roam all over the world.

The unpainted (or “white”) pallets are sometimes collected and resold, but nobody has much incentive for maintenance on them – and they are less well made.

The pallets come in standard sizes, but the standard size is different in Europe and America – the size coming from regulated truck sizes which in turn come from regulated road widths. Sometimes European pallets wind up in America, other times American pallets wind up in Europe and this complicates the recycling process.

There are a few independent pallet pools as well. There is one in Japan. There is no pallet pool in Iceland, but Iceland is awash in red and blue pallets that have found their way to the isolated island and often do not come back.

If you run a pallet pool you want it to be very geographically extensive – preferably running over the whole world but at least covering whole continents. You want this because there is network effect in collecting and recycling pallets. You also want to be a hard-nosed operator – happily renting pallets at low fees to businesses where the pallet is almost always effortlessly recovered, but willing to cut off any business that sends your pallets to uncollectible locations or damages your pallets.

The best customers are likely to be in the fast-moving consumer-goods suppliers as a pallet delivering breakfast cereal does not stay anywhere for long and the pallet is easy to recover. The worst customer is someone running a brick yard because the pallets will be damaged by the heavy loads and besides everything that winds up on a building site finds its way to the rubbish skip. Recycling is not a thing.

This desire for size and large networks makes a pallet pool business immune from competition from smaller pallet pool businesses, but they are not immune from competition with cheap “white” pallets.

The biggest pallet pool in the world (the blue ones) is called CHEP and is the only substantial business of Brambles, an old Australian diversified conglomerate. CHEP was originally the Commonwealth Equipment Handling Pool, and the pallets were left behind by the US military at the end of the Second World War. Brambles consolidated pallet pools globally.

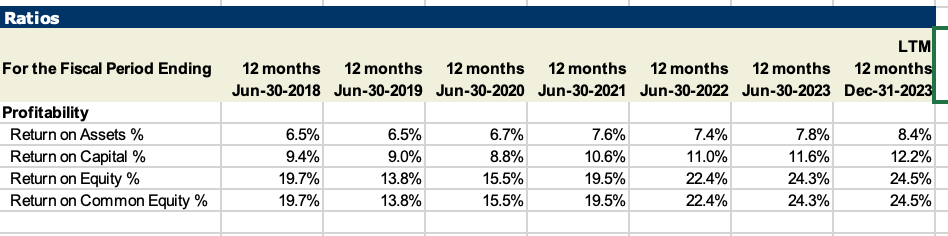

Being a natural monopoly Brambles has attractive looking returns on assets and returns on equity. Here are the recent ratios.

A return on equity of around 20 percent is not bad – and it has had that return on equity for most of the last twenty years. It looks like a good business, and it is surely okay.

The first observation though is that the return on assets is lower than you would like – and they get the high return on equity via some leverage. That is not surprising. This is a capital-intensive business. The pallet pool is well over 300 million pallets and whilst each pallet only costs something around $30 – the company has over USD9 billion in gross property plant and equipment on the balance sheet.

The second problem though is that the company has had massive (even insurmountable) problems in growing its high ROE network business beyond pallets. The history of non-pallet businesses detailed below is mixed. They have often deployed incrementally capital poorly.

Some history

When I started investing in shares (in the second half of the 1990s) Brambles was a diversified industrial services business. The pallet business was owned outright in Australia but much of the rest of the world was in joint ventures with GKN (a British engineering and aerospace company). The earliest annual report we have is 1995 – and the company self-describes as follows:

Brambles provides a wide range of services to industry including:

• Industrial equipment rental, ranging from rail wagons to forklifts and specialised access equipment.

• Pallet management and specialised container services.

• Industrial and contract mining services.

• Industrial and municipal waste collection, treatment and disposal.

• Specialised transport services, particularly dangerous goods and bulk raw materials.

• Records management and security transport.

• Marine services.

The idea that this would become a specialist pallet company was not broached at that time. They were building new businesses in airport services, but they were beginning to suffer competitive pressures in diverse areas – but especially in waste disposal.

In 1999 they were clearly committed to the multi-pronged business. They talked at length about the highly profitable French fork-lift rental business. The lesson that equipment rental businesses are super-cyclic was yet-to-be-learnt.[1]

By 2000 the annuls were still black-and-white affairs – but the pallet business had become the first amongst equals:

Brambles operates five global businesses: CHEP pallet and crate pools, Cleanaway waste management, Recall records management, contract industrial services (principally to the steel and mining industries) and a wide range of equipment rental services. The company also operates regional businesses such as marine services in Australia.

Returns on equity however were almost 20 percent and the company was growing nicely. The recipe for a stock-market-favourite was there. The stock was very highly valued at the time and the long period of underperformance since explains the distaste many Australian fund managers have to this stock.

The next year – 2001 – was the watershed year. GKN split into its equipment handling business and its engineering business – and the equipment handling business merged with Brambles to create what is now CHEP – the global pallet business. Also, the company realised that some of its businesses such as forklift rentals were not any good. They took over 200 million Australian dollars in write-downs including 195 million in equipment rentals.

Profits dropped by well over half, but modern Brambles was created.

By 2002 the goal of focussing on the good businesses was clearly stated:

We also sent a strong message to the market that the merged organisation would provide greater opportunities to foster growth in the core elements of the new economic entity called Brambles.

To position the Group for this growth phase, we undertook a portfolio audit to determine which businesses had the highest likelihood of continuing to create value into the future.

As shareholders will have observed, a number of non-core assets have been sold, as part of the process of refocusing Brambles on key, highly performing businesses. This, in turn, enables us to concentrate on developing our strongest business units.

At this stage the good businesses were CHEP, and a cleaning services business called “Cleanaway”. However, the future was CHEP:

Brambles’ new operating model has truly exposed the value drivers, particularly in CHEP.

Looking back at these annual reports you wonder how much it planned that they would focus on a business with a global network effect (being the biggest pallet rental company) and how much they stumbled into it as other businesses – such as fork-lift rentals in France – showed themselves to be awful.

In some sense we are not sure it matters. A good poker player often gets good by (a) limiting their bets, and (b) leaning into what works and away from what does not work. I know and respect a reasonable poker player turned portfolio manager who does this. His portfolio is almost theory-free. He really doesn’t care what works – but he manages his bets and is very skittish when things are no longer working. His returns are excellent.

Still in 2002 there were some businesses now that are comically different from Brambles current image.

Brambles these days positions itself as a “green” company – one whose core business is recycling (re-using pallets). In 2001 they were still talking about their new pulverised coal injection plant at BHP Steel Port Kembla which they described as a technological breakthrough. Indeed, it was the heap of coal which is the first colour photo in any of the annual reports in our archive.

That said they were divesting coastal shipping, railway car rentals, towing companies and all sorts of sub-scale businesses.

Still, leaning into the CHEP business caused problems. The pallets go everywhere, you do not know how many you need, and you don’t, at least at first, know which customers will ensure you get your pallets back. It is easy to sell at rental rates pallets to a brickworks – but you will make a loss as your well-built and moderately expensive pallet gets leased out at $5 to a company that will not return it. Those problems came home with a vengeance in 2003. To quote the annual:

As the repositioning of CHEP progressed, it quickly emerged that the previous high rates of growth were unsustainable. The level of capital required to fund this growth was placing undue strain on margins and the balance sheet. In addition, one of the key disciplines in managing a pallet pool – that is, control of the assets – had not been sufficiently rigorous. The correlation between the growth of the pallet pool and the commensurate growth in revenue had become increasingly disproportionate.

Over the past year, there has been an enormous effort to improve the asset productivity of the pallet pool. CHEP Europe has relocated 2.4 million pallets across the network to enhance utilisation rates. Physical audits led to another 1.1 million pallets being added back to our customers’ holdings, with associated revenue improvements, and customer deficits resulted in compensations being charged for another one million pallets. Provisions were made in relation to a further four million pallets that were written off as a result of this process.

In some sense the company is simply working out what does not work (leasing pallets to the wrong customers) and leaning away from it. But the losses along the way were not small.

The company set out a timeframe to fix these problems and mostly they did fix it. The next annual report isn’t quite triumphalist – but it is working, and they promise that they are going to step on the gas. They will lean (hard) into what is working.

By 2006 they had almost entirely lent into the CHEP business. They sold all their businesses except CHEP and document storage (and received USD3.6 billion). It was that capital that was to fund the expansion of CHEP.

Given the whole thing only has a market cap now of less than USD14 billion they have not done well since this transaction.

There was an acquisition that year – of AUSDOC – an Australian document handling and retrieval business.

By 2007 the company had started what was a poor period in capital allocation. The CHEP business was clearly working – so they thought that any other network pallet-style business might work. And they kept sinking capital into this idea.

The company claimed to own 235 million of the blue wooden pallets that are the core business – but there were 50 million other types of pallets, and they got all the photos in the annual report. There were pallets for the automotive industry, pallets for the fruit and vegetable industry, and later specialist containers for shipping chemicals. This was the new Brambles.

The annual report showed fruit-and-vegetable pallets – and they were made of plastic, and displayed on the floor of the grocer, something that becomes important later in the story.

Still, this is how the company ran for a while, sinking money into non-wooden-pallet businesses whilst still reporting good numbers. The plastic pallets, the chemical containers, the automotive boxes and all were bundled with CHEP so you could not see how the sub-businesses were faring.

The numbers even looked good during the global financial crisis – but they were helped by the currency they kept accounts in. The company reported in Australian dollars and the very weak Australian dollar hid a high single digit constant currency revenue decline.

Looking back on this period we are not sure that they were measuring what was working well. The segment called CHEP contained what we now know as CHEP but also a bunch of other businesses that clearly were not as good as CHEP. Also reporting in Australian dollars hid many of the cyclic nature of these businesses because the Australian dollar gets weak every time the global economy gets weak and so bad constant currency numbers in a downturn were flattered when measured.

If you are going to have a strategy of leaning into what is working and away from what is not working (a strategy we mostly endorse) you need to know what is working and you need to know it well. You need to have good systems to know your numbers. Otherwise, you wind up with the debacles as they unfolded in 2012.

We finalised and began to implement an exciting long-term growth strategy. In line with this strategy, we will focus on building our global equipment pooling solutions business by expanding into

more customer segments, diversifying our range of products and services and growing geographically, including in emerging markets. The IFCO acquisition has positioned Brambles as the leading global provider of reusable plastic crates (RPCs) to the fresh produce sector, complementing our position as the global leader in pallet pooling. We are particularly well placed to expand the RPC business in the USA, Europe and emerging markets.

They were sufficiently convinced of the scale advantages they had in pooling businesses that they sold their document handling business (under the combined name “Recall” to fund this growth). The buyer got a great deal.

Spending money on other than the core CHEP wooden pallet business was not a problem either.

We have identified incremental organic capital investments of US$550 million to expand our RPCs, Containers and emerging markets Pallets businesses further over the 2012 and 2013 financial years. Since our 2010 annual report, we have announced three small acquisitions in the containers sector, acquiring Unitpool and JMI Aerospace — to establish a global presence in aviation container pooling — and Container and Pooling Solutions (CAPS), a provider of intermediate bulk containers to the food, automotive and general industrial sectors in the USA.

In 2013 they continued this capital allocation strategy:

One highlight of this progress is our continued expansion of the global Intermediate Bulk Containers (IBCs) business following the acquisition in December 2012 of Pallecon, an IBC pooling services provider with more than 30 years’ operating experience. We have now merged Pallecon’s operations in Europe and the Asia-Pacific with the IBC operations of CHEP and the CAPS business in North America to form CHEP Pallecon Solutions.

By the 2014 annual the bold assertion that we have won in wooden pallets so we can win in all other categories has disappeared. The company is reporting in US Dollars (which removes one mismeasurement problem) and breaking out the returns after a capital charge by the type of pallet they are using. Here are the numbers:

They meet their cost of capital (easily) in wooden pallets, and they just don’t in plastic containers. They are also promising cost-cutting, but they are not yet undoing the mistake of leaning into things that do not work. That said – there is an important acknowledgement here – the reusable plastic container business does not meet its cost of capital, and it is getting worse. The idea that Brambles was inherently good at pooling containers is just false.

You would think that acknowledgement would change management strategy, but it did not. They simply did more of the bad stuff in the 2015 financial year.

In September 2014, we acquired Ferguson Group, a leading provider of container management solutions to the offshore oil and gas sector, for US$523 million. This acquisition represented an opportunity for Brambles to enter a new supply chain, which has attractive long-term characteristics and in which we believe we can create value through our extensive and longstanding equipment-pooling expertise. We anticipate any acquisitions in 2016 will be in support of our existing businesses and will be relatively small and accretive, such as the Rentapack and IFCO Japan acquisitions we have completed in recent months.

The accounts again admit that none of these new businesses meet their cost of capital – but nothing much is done about it. They have a review in the following year, but they are still sinking capital into these businesses at a rapid clip. They merge the oil-and-gas-crate business but continue to own 50 percent of the merged business and think there will be more opportunities.

They sold a profitable and quite nice logistics software business though. You wish they were just pragmatic here – leaning into what works, leaning away from what does not work. But it isn’t like that. They are doubling down on what doesn’t work and not talking about it.

2018 brings a new CEO, Graham Chipchase – who is still there, and foreshadows a new Chairman. That is usually a time of some change, especially when you have underperforming businesses. And there is change – but it starts quite considered. The key development is that they break up the pooling businesses into segments, the post important being plastic containers (IFCO) and the CHEP business. This is announced innocuously enough.

Our decision to separate IFCO is in line with our strategic priorities. Although both CHEP and IFCO are pooling businesses, they are materially different in nature, with distinct financial profiles, offerings and customer bases. There is limited operational overlap and no material customer-related synergies that will be lost on separation. As separate entities, Brambles and IFCO will have greater focus on their distinct strategic agendas and increased flexibility to pursue growth opportunities. For shareholders, a separation provides focused investments in two world-class, global businesses that are positioned for long-term success.

This however is throwing down the gauntlet for the management of the non-wooden pallet businesses. You need to meet your cost of capital now unsupported by the really good wooden pallet business or you are going to be sold. The new CEO does not immediately dismantle the old strategy – but he lays the groundwork by which it will be dismantled.

It does not take long. They sell the underperforming plastic pallet business and surprisingly they get a nice gain on sale. (It is better to cash your losers in a bull market.)[2] They return most of this money to shareholders with a special dividend and buybacks. This is now a smaller, but we think better business – and it has become the Brambles we know today.

The next year the Chairman changes too, to John Mullen. Mullen appears to be a steadying influence – but the change of strategy happened with the new CEO appointed before the new Chair arrived.[3]

What are we left with?

We are left with a business with a history of mild mismanagement and not much trust in the Australian market. The stock was hugely rated in the early 2000s. It is now traded at a sub-market price to earnings ratio. It is however back to the core and only consistently good business – blue pallets in massive pools.

We think that is a fairly low risk position – but there are caveats we discuss below.

And we think the management team are appropriately modest – realising that the company has been inappropriately adventurous in the past. Moreover focus (as opposed to diversification) is fashionable in management circles these days – and given the history of this company that seems appropriate.

Plastic pallets and Costco

Most pallets that go to retailers such as Walmart never see an end retail customer. The pallets are delivered to the storeroom at the back of the retailer and the stock is shifted in boxes to the shelves.

This is not the case at Costco (or sometimes Aldi) where the pallet of breakfast cereal or the like are put directly on the floor. The pallet is furniture.

And if is furniture the retailer would like it to be clean – without splinters or worse nails which customers could hurt themselves with. Costco is particularly strong on this.

Costco wants plastic pallets.

Plastic pallets however are considerably more expensive than wooden ones. They are more durable but more likely to go missing. They would involve a substantial capital investment to introduce plastic pallets to the pool and manage them accordingly. The cost of replacing the entire pool with plastic pallets would exceed USD30 billion. That is not readily conceivable.

The most common question posed in the press about Brambles was would CHEP supply Costco. Given the experience above with plastic containers displayed on grocery shelves (as per the picture) the answer was unsurprisingly no.

This is risky. Someone might start a rival pallet pool and hence damage CHEPs business. Analysts did not seem to like Brambles’ refusal to deal with Costco. On this one however we will defer to the management and the history. We are pleased management was reluctant to repeat past mistakes.

Poisonous relationships in the supply chain and a partial technological fix

A key feature of a pallet leasing business is that you do not want to lease pallets to just anybody. CHEP has lost money multiple times with bad leasing deals – though we have not spotted any bad deals lately.

We once went into a warehouse that was storing half the sugar beet seeds that were likely to be used in the world in the next year. It was about the size of a football field stocked to a high ceiling with pallets holding containers of sugar beet seeds. They were stored for most of a year and the pallets in that warehouse turned over once a year.

Unsurprisingly they were not painted red or blue. A pallet leasing company does not want to lease pallets to someone who will return them a year later.

But there are other undesirable customers. Famously CHEP tracked many unreturned pallets to Bunnings – a Home Depot style hardware chain in Australia. The unreturned pallets were used as furnishings in the garden centre – sitting in the rain with garden pots and plants on them – trashed as the weather eventually destroyed them. CHEP sued for unpaid lease fees and won. Now Bunnings has a sign at its warehouse that it will not accept any goods consigned on a blue pallet. The relationship is unconstructive for both parties.[4]

But this is also key to how you run a pallet pool. If you lease $30 pallets for $5 you must get them back to make a profit. And fixing your relationship with parties that do not return pallets is a key management priority.

But first you need to know who does not return pallets – and that is hard because pallets roam over the whole world and the person who you deliver the pallet to is not the person who returns it.

Modern technology helps. A tracking device that you stick on a pallet, and which pips out its GPS location a few times a day now costs USD60. This is twice what the pallet is worth. But if you stick a hundred thousand of these in your pool of 330 million pallets you will find out a fair bit more about the path these roaming pallets take. (You might also work out your loss rate more accurately.)

But knowledge of missing pallets will leave some gnarly business management issues.

For example, there are thousands of small businesses that collect pallets. They take them to their central store yards (there are several in every big city), sort them into red ones, blue ones and white label ones. If they can resell the white label ones they can make a good living. They also get paid a fee by CHEP for collecting blue pallets and returning them to CHEP or better taking them to CHEPs next customer and clipping the leasing fee.

Alas some of these businesses (detailed in a story in the WSJ) were building their stockyards to hide the blue pallets and they were selling blue pallets to customers CHEP did not want (such as building materials) or to CHEP’s own customers and were collecting the leasing fee themselves. Obviously CHEP would like to be paid for their own pallets, but equally obviously CHEP wants to keep the small-time pallet recyclers happy. CHEP are not physically everywhere and if a small business does a run collecting pallets, they should be happy (as long as they collect their share of the lease fees). Negotiations will be required. This better be conducted more delicately than the negotiations with Bunnings.

COVID and CHEP

It was COVID and its aftermath that made us particularly interested in Brambles. The wooden pallet business was far more affected than you would expect.

There were two big things that happened.

a). the lumber price went up a lot, and then up some more. This made pallets far more expensive, meaning that the capital cost went up for Brambles (by a lot) but also customers were far keener to rent pallets rather than buy white label pallets.

b). supply chains lengthened meaning many more pallets were stuck in the system and not getting returned to CHEP. CHEP and its customers found themselves short of pallets often imposing quite substantial costs.

The starting gun for our interest was a friend of the firm who has a business importing exotic liquor into the United States. One of his products is Brenavin – an aquavit which is effectively the national spirit of Iceland.

He could not get pallets; hence he could not export liquor from Iceland. The simple absence of pallets collapsed his business. When he could get pallets, the price was sky-high – enough to substantially erode his margins.

He was also “buying” blue pallets in Iceland. This was unusual because CHEP has no operations in Iceland. Though in this case he was sending the blue pallets back to America where presumably one day CHEP would collect them. We guess CHEP should be grateful for that.

This story was repeated around the world. Truck deliveries which used to take a week took three weeks as warehouses backed up. The number of pallets stuck in transit expanded. The pallet shortage was exacerbated because businesses scared of running out of pallets stockpiled them.

CHEP had to add tens of millions more pallets than normal to its pool. Unfortunately, it had to do this with sky-high lumber prices. Moreover, most pallet rental contracts have terms about three years, and they could not immediately pass the costs of this onto their customers. The company went cash flow negative because of the sharply increased capital expenditure.

CHEP was so short of pallets at the time that they literally stopped signing on new customers.

The out years should however be good. CHEP never failed to deliver pallets to customers (though they often had to run extra trucks to collect pallets and move them around). The lesson was learned: if you have a CHEP contract you are not going to run out of pallets – and pallets are mission critical. So CHEP should find it easier to find new customers in the future and should be able to charge those customers more for reliability.

Also, CHEP over-invested in pallets when supply chains were stretched. They will need to invest in fewer pallets in the future. Cash flow should be better. Also, the technology changes described above should improve the tracking of pallets and hence pallet losses. This should also improve cash flow.

There is in our view a good chance the next few years are better than the past, and that is why we own the stock.

A name change for Brambles?

The Brambles name is historic, going back to xxx. The name has a storied history in Australia and everyone who has been involved in Australian stocks knows this name.

But the old Brambles was a conglomerate – an asset trader which often traded asset badly. And the name still stands for that.

These days Brambles has a single business in which it is a global leader and on which its efforts should be focussed.

We have never met the board chair (John Mullen). I would like to. Mostly though we want to suggest a single symbolic change. We suggest that the company change its name to CHEP. We want this to make sure that Brambles never falls back into the conglomerate asset-trading mentality of its past. It is a small change, and merely symbolic. It would cement what we think is a good direction.

Finally - a call for comments

I put this on the blog mostly so people can point out where I am wrong. I am betting here that the past (disappointment, capital mismanagement) will be different from the future - and that is obvious. But other thoughts would be appreciated.

John

[1] An equipment leasing business which meets customers marginal needs can be disastrously cyclic. Imagine if the customer owns say 80 percent of their forklifts – the forklifts they might need for work in a recessed economy. In a boom they rent the marginal forklifts from an operator like Brambles. Then when a recession comes, they keep their own forklifts and return all the rented ones. The rental equipment company is left with debt used to finance forklifts now rusting in their yard. This business can be disastrous.

[2] Needless to say other bits of the business dismantled did not work so well.

[3] For the observant, Mullen has a similar problem at Qantas. Qantas went from good to disastrous under its past Chairman and CEO. The board is conveniently blaming all the problems on the now departed CEO. A new CEO has been appointed before Mullen arrived as Chair. He must work out whether what he inherited is now on the right direction or whether it is time for another shakeup. We think he did a good job at Brambles, but Qantas is a much harder situation. [PS. If any readers know him – please show him this. I would love to chat.]

[4] Shareholders of both companies should deliver gifts to any management teams that fix this relationship.

Thanks for the insightful post, John.

Isn't CHEP a business where the accounting inherently flatters the true economics of the business?

Pallets are assumed to have a useful life of 10 years. Their provision for lost pooling equipment ('IPEP' expense) was $185.5m in FY'24 (~3% of plant & equipment). Based on your post, it sounds like they can't accurately track this 'lost pallet' figure, so both the useful life and the loss rates of the pallets could be materially worse than assumed. At any rate, total capex in the continuing operations was $1 billion in FY'24, notably higher than depreciation. This seems to have been the case stretching back many years, even adjusting for the spike in timber prices (capex-to-sales for FY'24 was at its lowest level in 5 years).

On a cash basis, the returns on capital/equity are lower than you cite and, conversely, the valuation multiples are higher. Perhaps CHEP/Brambles is only a 'good' business if judged by the accountants, but may not even be 'okay' as judged by the cash register?

XXX = 1875.