Focus Media: My new obsession - original version with annotations

There are days I should not be allowed to hang around a spreadsheet. This post had not one but two - nearly identical mistakes in it. I simply read off the wrong line in my tables and quoted gross margins not operating margins. I have corrected below and put in an addendum with the original sources of the correct data in it. I have also republished the post as it should have been in the first place.

Just to make it clear - phrases removed from this post are in strike through and additions are in italics.

If you have not read this post - just go straight to the corrected versions.

The announced "go-private" transaction for Focus Media has me obsessed. It seems to cover a whole gamut of my interests, Asian private equity, alleged Chinese fraud, connections with major property developers and numbers and accounts I find surprising. The whole works! It may not be the most important thing in financial markets this year - but it is one of the most interesting.

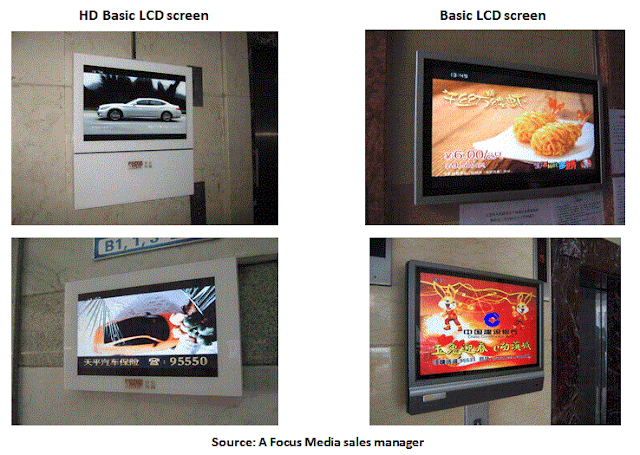

Readers might need some background here. Focus Media is a display advertising business in China which has analogue and digital poster frames in elevators and shopping centers as well as LCD screens placing advertisements more generally. Most of these adverts are small (the LCD screens are mostly 17 inch according to the annual report and many of the posters are smaller). Here are pictures of a few...

(My source for these photos is a Seeking Alpha bull on the stock here...)

A lot of what used to be counted as LCD screens are simple posters:

The reason for using posters is inconveniences like having no available power supply. There has been some dispute about the number of screens and posters but there is no doubt that the company has a lot of these - they are visible around major cities in China.

The company also claims to have the right to sell advertising on a large number of movie cinema screens. Again there is a dispute about the number of these screens.

The mechanics of Focus's business

Focus Media is a relatively simple business. They rent sites (for instance by entering a lease with the managers of a large tower with elevators they wish to place adverts in). They sell the advertising space and they maintain all their screens and update your posters and deal with the inevitable things like vandalism, theft and the like. For the number of sites that Focus deals with they would need a fairly large number of lowly paid staff for maintenance and another group of staff selling advertisements and a third group negotiating lease arrangements with building and cinema owners. The second and third group will have higher salaries.

The maintenance cannot be neglected because it devalues adverts when kids scrawl little goatie-beards on the pictured women (or worse).

The profitability of Focus's business

The most notable thing about Focus from the accounts is their startling profitability. Their last annual report shows revenues (net of business taxes) of USD793 million and operating gross profit of 503 million, operating profit is 259 million. This is an operating of margin of 32.7 percent in a which is at the high end for a media business. In my experience media businesses are 10-35 percent margin businesses - with the high numbers reserved for very special franchises. A monopoly newspaper in a city of a million people (say Perth Australia) used to have a 35 percent margin before the internet threatened the monopoly. Most businesses are closer 20 percent. Most display advertising businesses (which are without strongly identifiable franchises) earn closer to 10 percent margins.

Moreover, this is a 63 a 33 percent margin where the company itself describes the landscape as "competitive" in their annual filings. The margins are surprising – but China is a surprising place in many ways – and it is possible that margins are fat because the landlords who lease the space to Focus are stupid. The fat margins may be possible for other reasons I don't understand.

First let me stress though just how fat these margins are. The largest player globally in display advertising is JCDecaux (the French multinational founded by Jean-Claude Decaux). They have - according to their last accounts - €2463 million in revenue and 23.6 percent operating gross margins. The 63 percent gross margin at Focus is fully 40 percentage points higher than the gross margin of JCDecaux. The net margin of JCDecaux is a mere 8.7 percent - Focus Media margins are 3.7 times higher than JCDecaux.

Moreover JCDecaux has fatter and thinner margin businesses. It has a mid teens operating gross margin outside their (franchise) street furniture business.

There are several possible explanations for the very fat margins at Focus. The most obvious explanation is that they were early... when you go around to a landlord and offer to rent their space they don't know what that space is worth (because the idea is new to them) and they lease it to you for too little. Over time margins contract because the landlords "wise-up". This is certainly true in the street-furniture business at JCDecaux where the company goes to the local government and offers to maintain their bus-stops for "nothing" and the local government (with the intellectual panache that describes that sector) just accepts. But local governments have wised up over time.

The bears in this stock - and there are many (see the many seeking alpha articles) - would suggest the margins are made up. As an outsider that is pretty hard to test - but going through the claims and counter-claims with a fine comb is the sort of thing that excites a guy like me. (Any private equity party doing thorough due diligence can check those claims.)

The main fraud allegation

The main allegation against Focus came from Muddy Waters - the same firm that exposed the fraud at Sino Forest. MW gave us an 80 page report (that is freely available on their website). Sino-Forest was deep within my area of expertise and I was more-or-less instantly convinced that the whole Sino Forest story was made up. Focus Media is a much harder target for Muddy Waters because the company clearly exists. Their LCD screens and picture frames are pervasive in many large cities in China.

Whilst I was instantly convinced by the Sino Forest case (and hence was happy to short the stock to zero) it is harder to be convinced when the business so clearly does exist.

That said Carson Block and his Muddy Waters firm comes with some credibility because they predicated the complete demise of Rhino International and Sino Forest (both multi-billion dollar firms). Given Carson's street-cred I was surprised that Focus Media stock held up so well after Carson's attack.

Some people clearly saw a lot of value in Focus even if some part of Carson's allegations was correct.

The private equity bid for Focus

The people who saw value in Focus Equity include some of the most important private equity firms operating in Asia who are bidding for the whole company. Here is the release:

Aug.13, 2012 -- Focus Media Holding Limited ("Focus Media") today announced that its Board of Directors has received a preliminary non-binding proposal letter, dated August 12, 2012, from affiliates of FountainVest Partners, The Carlyle Group, CITIC Capital Partners, CDH Investments and China Everbright Limited and Mr. Jason Nanchun Jiang, Chairman of the Board and Chief Executive Officer of Focus Media, and his affiliates (together, the "Consortium Members"), that proposes a "going-private" transaction for $27.00 in cash per American depositary share, or $5.40 in cash per ordinary share...

The bidders are a who-is-who of reputable private equity firms. FountainVest is run by Frank Tang who used to head China investments for Temasek (the Singapore Sovereign Wealth Fund). He represents Singapore Inc as much as a private individual can. The Carlyle Group is one of the largest private equity firms in the world. I have had my doubts about their China investments before - but they are large and reputable. CITIC Capital is a private equity firm associated with China International Trust and Investment Corporation which is effectively the Chinese sovereign wealth fund. CITIC Capital however is not the Sovereign Fund - rather an associated private fund. By all accounts it is Princeling Central. China Everbright is a Hong Kong listed financial firm clearly with links to the Chinese establishment. Bo Xilai's brother recently quit as a director. This group is a mix of Chinese, other Asian and Western establishment firms.

One bank mentioned in the press release is DBS - which again represents Singapore Inc. The only other bank mentioned is Citigroup - and they have provided a "confident" letter.

So where are we now?

What we have are some high-profile but rat-bag shorts on one side squealing fraud. And on the other side we have a who's who of Asian business wanting to take this private for the not-so-trivial sum of USD3.5 billion.

You see why I am obsessed? Right up my alley. And perhaps a test of my Guanxi vs Analyst thesis.

Is this a done deal?

This sounds like a done-deal. The largest shareholder in Focus is Fosun International - an HK conglomerate. They have publicly called the bid "attractive". The bid team contains Mr. Jason Nanchun Jiang - the CEO/Founder of Focus - and a man critical to the running of the business (apart from anything he controls the variable interest entity). Given that it contains the critical person and the main shareholder wants to accept it is likely the board will go along. And the bid is cheap enough that it is unlikely that - absent absolutely grotesque fraud - nothing that is found on due diligence will dissuade the buyers.

The parties are rich enough that $3.5 billion is a big - but not an intolerably large bite. They are up for it.

It is however subject to due diligence. The letter sent by the buyers to the company is attached to the press release. The last paragraph says it clearly:

13. No Binding Commitment. This letter constitutes only a preliminary indication of our interest, and does not constitute any binding commitment with respect to the Acquisition. A binding commitment will result only from the execution of Definitive Agreements, and then will be on terms and conditions provided in such documentation.

And so we have a due-diligence period in which some of the most reputable and largest private equity firms will do due diligence on a company that one of the most famous rat-bag short-sellers asserts is a fraud.

Oh to be a fly-on-the-wall

I would love to be a fly-on-the-wall as they work out how to test the Muddy Waters allegations. Due diligence is sometimes (incorrectly) treated as a formality. But in this case the stakes are real. Billions of dollars are on the line and the very credibility of some firms (especially Carlye) are on the line with it. Carlyle has been burnt by some frauds in Asia before. If - after warning by Muddy Waters - Carlyle were to buy this firm and it turned out to be fraudulent the question would arise as to whether Carlyle staff were deliberately buying frauds to loot the Carlyle funds. My guess is that the very existence of Carlyle is at stake.

But Carlyle have competent staff laced throughout their organization. They will do their due diligence - and if the deal closes I think you can presume that Muddy Waters was wrong.

If the deal doesn't close with the backing of the the largest shareholder and at this pricing then you probably have to conclude that Muddy Waters is right. If Muddy Waters is right then the revenue and the margins of this firm are grotesquely overstated and the stock is probably going to settle somewhere below two dollars.

And with that you understand my obsession.

John

Disclosure: I think there is a reasonable chance that Carlyle - and perhaps some of the other firms in this syndicate will walk. In all honesty I have no idea whether they will or not but as the stock will wind up at $2 (or less) if they walk the bet is worth taking. So I am short and risk losing the difference between the current price (25 and change) and the bid price (27) if the deal does close.

============

Data sources for the addendum:

Here is the P&L for Focus Media from the last annual report:

FOCUS MEDIA HOLDING LIMITEDCONSOLIDATED STATEMENTS OF OPERATIONS

For the years ended December 31, 200920102011 (In U.S. Dollars, except share and per share data,

unless otherwise stated)Net revenues $397,164,522 $516,314,697 $792,620,177

Cost of revenues 241,073,203 221,690,034 289,644,266

Gross profit 156,091,319 294,624,663 502,975,911

Operating expenses: General and administrative 88,833,305 79,759,757 127,012,894 Selling and marketing 79,786,861 103,722,237 147,716,437 Impairment loss 63,646,227 5,736,134 — Other operating expenses (income), net 13,111,043 (14,143,945) (16,137,695)

Total operating expenses 245,377,436 175,074,183 258,591,636

Income (loss) from operations (89,286,117) 119,550,480 244,384,275 Interest income 4,945,946 7,259,508 15,538,943 Interest expense — — 716,956 Investment loss — 1,287,881 —

Income (loss) from continuing operations before income taxes (84,340,171) 125,522,107 259,206,262 Income taxes 13,780,065 22,335,579 54,761,394 Loss from equity method investment — — 43,632,613

Net income (loss) from continuing operations (98,120,236) 103,186,528 160,812,255 Net income (loss) from discontinued operations, net of tax (111,612,420) 83,077,575 —

Net income (loss) (209,732,656) 186,264,103 160,812,255 Less: Net income (loss) attributable to noncontrolling interests 3,524,388 1,990,626 (1,864,783)

Net income (loss) attributable to Focus Media Holding Limited Shareholders $(213,257,044) $184,273,477 $162,677,038

Income (loss) per share from continuing operations — basic $(0.15) $0.15 $0.24

Income (loss) per share from continuing operations — diluted $(0.15) $0.14 $0.23

Income (loss) per share from discontinued operations — basic $(0.17) $0.12 $—

Income (loss) per share from discontinued operations — diluted $(0.17) $0.11 $—

Income (loss) per share — basic $(0.33) $0.26 $0.24

Income (loss) per share — diluted $(0.33) $0.25 $0.23

Shares used in calculating basic income (loss) per share 651,654,345 707,846,570 671,401,000

Shares used in calculating diluted income (loss) per share 651,654,345 731,658,265 693,971,258

The accompanying notes are an integral part of these consolidated financial statements.

And here is JCDecaux's P&L - snapshot picture from their annual report...