Japanese regional banks - a mirror on America

77 Bank is a regional bank in Sendai (the capital of Miyagi prefecture). The Japanese guys I know think of Sendai as a backwater – a place where the “cool guys” hang out on motorcycles wearing purple clothes. Economically it is just another rapidly aging backwater where the young (other than those that hang out on motor cycles wearing purple clothes) are moving to Tokyo.

The name 77 Bank harks to tradition. During the Meiji restoration the Emperor gave out numbered bank charters. Traditional regional banks still label themselves by the number. www.77.co.jp and many other numbered sites belong to banks.

77 Bank has a very large market share (near 50%) in Sendai. The market is more concentrated that the great oligopoly banking markets of Canada, Australia, Sweden etc. It should be profitable – but isn’t.

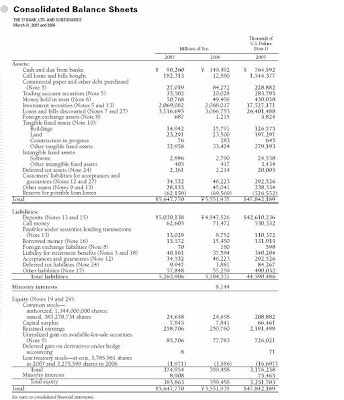

Here is its balance sheet:

(click for a more detailed view).

Note that it has USD42.6 billion in deposits. This compares to $35.8 billion for Zions Bancorp – as close to an American equivalent as I can find.

77 only has USD26.4 billion in loans though. If you take out the low margin quasi-government loans it probably has only USD20 billion in loans.

This bank seems to be very good at taking deposits – but can’t seem to lend money.

This is typical in regional Japan. It is also a problem – because when interest rates are (effectively) zero the value of a deposit franchise is also effectively zero.

So – guess what. It sits there – just sits – with huge yen securities (yields of about 50bps) doing nothing much.

It’s a big bank. It has next to no loan losses because it has no lending.

Here is an income statement:

(click for a more detailed view)

Profits were USD87 million on shareholder equity of 3251 million. You don’t need a calculator – that is a lousy return on equity for a bank without credit losses.

You might think that given that they have no profitability and no lending potential they might be returning cash to shareholders. Obviously you are new to Japan. Profits are 27 yen per share and the dividend is 7 (which they thoughtfully increased from 6).

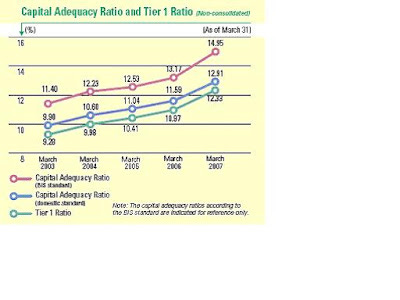

In a world where banks everywhere are short of capital 77 bank is swimming in it. Here is the graph of capital ratios over time:

This bank has an embarrassment of riches – and nothing to do with them.

Welcome to regional Japan.

An American Mirror

The title of this post was “An American Mirror”. And so far I have not mentioned America.

America is a land with little in deposits and considerable lending. There are similar lands – such as Spain, the UK, Australia, New Zealand and Iceland.

There are also mirror image lands – 77 is our mirror image.

Macroeconomic investing calls

We live in a world with considerable excess (mostly Asian) savings. Banks with access to borrowers made good margins because the borrowers were in short supply. Savers (or banks with access to savers) were willing to fund aggressive Western lenders on low spreads.

77 Bank has been the recipient of those low spreads. It has not been a fun place for shareholders as the sub 3% return on equity attests.

The economics of 77 Bank (and many like it) will change if the world becomes short on savings. There is NO evidence that that is happening now – and so 77 Bank will probably remain a lousy place for shareholders.

The market produces what the market wants

This is an aside really. We live in a world with an excess of savings. This is equivalent to saying that we live in a world with a shortage of (credit) worthy borrowers. So we started lending to unworthy borrowers – what Charlie Munger described as the “unworthy poor [whoever they might be] and the overstretched rich”. We know how that ended.

Unfortunately the financial system cannot make worthy borrowers. It can only lend to them when it can identify them.

This Subprime meltdown heralds the death (for now) of lending to the unworthy. The shortage of the worthy however is as acute as ever – and money for the worthy is still very cheap.

The subprime meltdown does not solve 77’s problems.