Purecycle and the good money after bad decision...

Has anyone got a hundred and twenty five million to help out a needy hedge fund?

One of the most read posts I ever wrote was one that asked the question: when should you average down?

The issue was a conflict between the two pieces of market advice that mattered. One was Warren Buffett’s famous aphorism that if you liked it at $10 you should love it at $6.

The other was Paul Tudor Jones famous admonition that losers average losers.

The conclusion that I reached (with some nuance) is that averaging down is generally okay when catastrophic results (a zero) are off the table. But if you average down into things that can go to zero you will buy a full position (say 7 percent of your book) at $50, a bit more at $35, some more at $20, more at $10 and soon you have lost 18 percent of your book on a 7 percent position.

Today though I get to look at the decision from the perspective of a hedge fund manager who has - alas - overcommitted.

Purecycle

Purecycle is a company with a claimed (but not yet demonstrated to run sustainably at scale) technology for recycling plastic. They had a desktop demonstration that worked, and released a dinky video claiming they got product out of their full scale plant, but they have yet to run the plant sustainably and generate substantial revenue.

The company has been running out of money too. The plant is late and over-budget. That doesn’t mean it will fail. It is just late and over-budget.

That is a problem though because the company has a whole lot of debt where covenants require the plant to produce at high capacity for a month by a certain date. A date which has now passed and was extended and which is fast approaching again.

The original short case against Purecycle

Hindenburg - a short research firm which is usually very good indeed - put out an extensive short report on Purecycle. You can find that report here.

I was also short Purecycle because of the association with certain people - people who have mostly left the company now - so my short case is considerably weaker than when I started. That said I remain short in my usual small quantity.

Purecycle and Sylebra Capital

Purecycle’s largest shareholder is Sylebra Capital and Purecycle is Sylebra’s largest position. Sylebra has properly hitched itself to the Purecycle bandwagon. They are in for above half a billion dollars. I have not calculated the total amount but by March 2021 (with the stock around $30) Sylebra had 17 million shares and they have continued to add.

Purecycle ran low on money in March 2022 and Sylebra added money to pot as per this linked press release. To quote: “the Offering included subscription agreements with Sylebra Capital, Samlyn Capital, and partner SK geo centric.’

Early this year Purecycle tripped its debt covenants. (The plant was not working at the required pace.) Sylebra stepped up again. To quote the form 10K:

Sylebra Credit Facility On March 15, 2023, PCT entered into a $150 million revolving credit facility (the “Revolving Credit Facility”) pursuant to a Credit Agreement (the “Revolving Credit Agreement”) dated as of March 15, 2023, with PureCycle Technologies Holdings Corp. and PureCycle Technologies, LLC (the “Guarantors”), Sylebra Capital Partners Master Fund, LTD, Sylebra Capital Parc Master Fund, and Sylebra Capital Menlo Master Fund (collectively, the “Lenders”), and Madison Pacific Trust Limited (the “Administrative Agent”), which matures on June 30, 2024. The Lenders and their affiliates are greater than 5% beneficial owners of PCT. Borrowings under the Revolving Credit Agreement may be used for working capital, capital expenditures and other general corporate purposes and satisfies the financing obligation imposed upon PCT by the Limited Waiver.

There was another term loan after quarter end. To quote:

Additionally, the Company secured a $40 million term loan with an entity controlled by Dan Gibson, the Chief Investment Officer of Sylebra Capital, PureCycle's largest shareholder. The loan matures on December 31, 2025, and bears interest at a floating rate of SOFR + 7.5%.

Whatever - at this point Sylebra Capital is in this one pretty hard.

Incentives on Sylebra Capital

At this point Sylebra has tied its existence to Purecycle. Whether that is smart or not is beyond the point. Purecycle may still work and it might even still be a home run for Sylebra.

Yes he broke my rule about doubling-down. And that may have consequences. But if Purecycle fails now Sylebra will probably fail with it. (The clients might reasonably be a touch jaundiced).

And if Purecycle succeeds Sylebra will look like heroes.

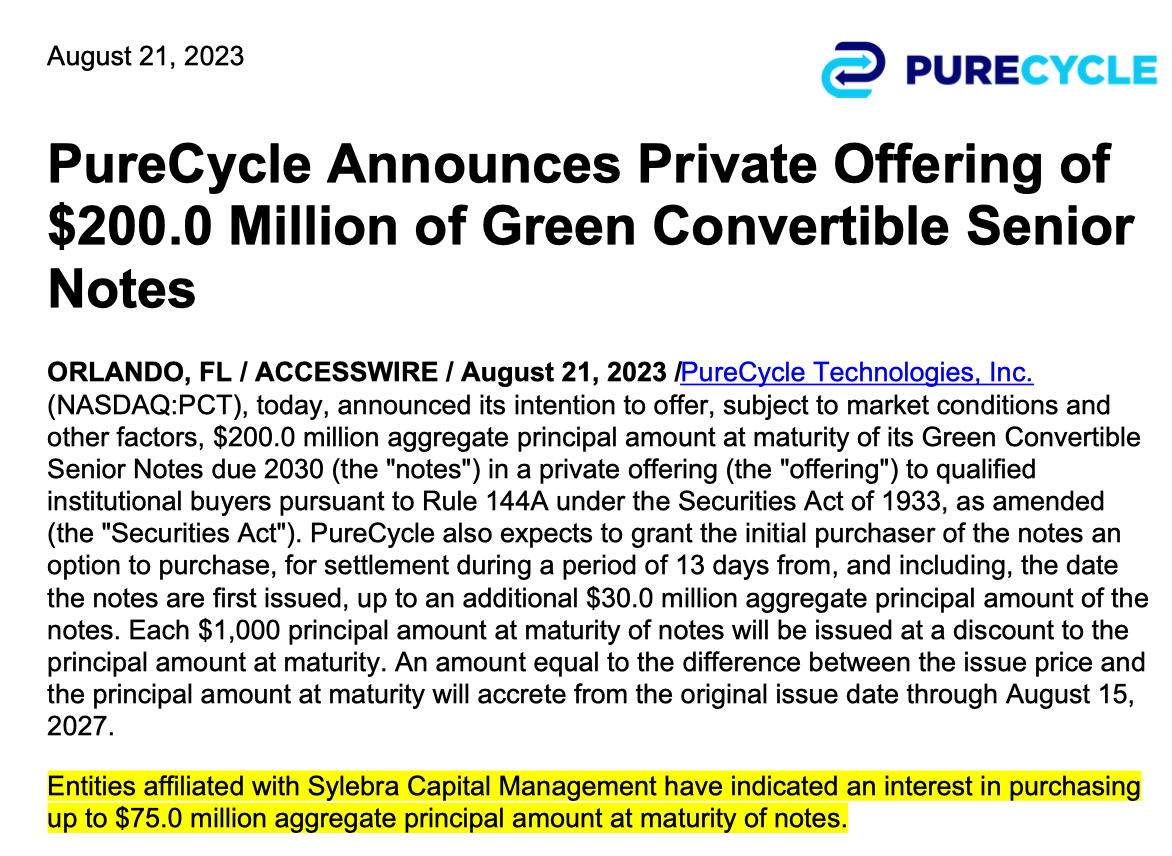

And here the asymmetry of rewards kicks in. Because Purecycle is out-of-money again they are issuing a $200 million convert.

If Purecycle runs out of money Sylebra is probably dead - but Sylebra is playing with client money. And so they can roll the dice again.

Heads they win.

Tails they just lose a bucket more client money but they are no worse off. (Sylebra is a basket case either way.)

So of course they are going to roll the dice. You can see that in today’s press release.

Now if it were there own money I might admonish them for throwing good money after bad. But it is client money - and unless Purecycle survives Sylebra is just done.

My rule about doubling down does not necessarily imply when you are done-for.

So why ins’t Sylebra putting up the whole 200 million?

The sharp-eyed will notice that Sylebra is only going to put up $75 million of the required $200 million.

Why not more? I don’t know but at a guess I would think they are nearing either risk limits embedded in their documents or they are cold out of liquidity.

Maybe they are just hoping for third party money to repay money they have previously lent to Purecycle.

To make this deal work - and to save Sylebra some other funds have to come up with the $125 million not being underwritten by Sylebra. That is on a deal which I think will rapidly default. After all they have about seven weeks until they trip their covenants again.

Maybe other people will have a different opinion and think this is money good.

Just maybe someone - out of an unusual sense of generosity - can come up with $125 million to help a poor hedge fund out.

John

We need a refresh in light of today's news!

Very interesting article. What is your tecnic in shorting stock. Do you short directly the stock or do you use options? In this case what strategy do you use? (bear call spread? bull call spread?)

Thank you