Time for Discover

Financial stocks in the US have been very weak.

The consensus is that the situation is bad on credit. I suspect the situation is more likely to be bad on revenue - but either way the consensus is bad for financials.

I am going to give you an anti-consensus set of charts. This is credit data on Discover Financial Services (NYSE:DFS) from their master-trust for their credit card products. The information is from indispensable Portales Partners. They do not like people redistributing their stuff - but I hope they are happy with an advert: if you run a serious amount of money in North American Financials you should subscribe to them. They are likely to make you think.*

Here is the last ten years of DFS delinquency data:

Note that delinquency is near a ten year low.

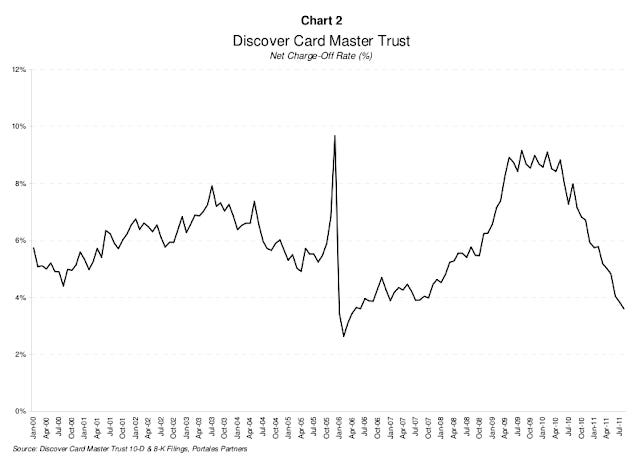

And here is the charge-off data:

The spike and the collapse in the numbers in the middle of the sequence is the change in personal bankruptcy laws which gave people an incentive to bring forward bankruptcy filings. This meant a spike and subsequent drop.

Net of the spike which was caused by a policy change the charge-offs are about the lowest in a decade.

Delinquency leads charge-offs so given the delinquency is low you would expect the charge-off to drop.

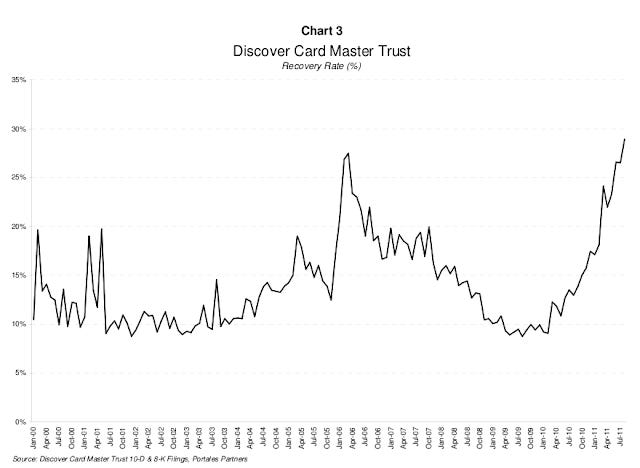

Some of the low charge-offs are caused by high recovery of past written-off debts (recoveries count as negative charge-offs).

Recoveries have come back to a high level.

Observation

DFS are reporting among their best credit numbers in a decade - and they are reporting it in a very sour economy. If the delinquencies really are a leading indicator these numbers will be the best in a decade shortly.

So what is happening?

I can see three broad possibilities:

(a) The numbers are not real - DFS is faking it.

(b). The numbers are real but they are DFS specific and they relate to changes in DFS policy such as a dramatic tightening of credit standards, or

(c) The numbers are real and middle American unsecured credit has improved dramatically despite the recession because consumers have retrenched and really are paying back their loans.

I will leave it to my commentators - you are a smart and well connected lot - to work out which.

But if it is (a) then DFS is a strong sell, and if it is (b) DFS is a strong buy. If it is (c) then there are a wide range of financial stocks you should buy.

John

*Seriously - this advert is warranted. Portales really are one of the better specialist firms out there.

Post Script

I know I am cheating with this list of choices - there are other possibilities like

(d) It is all going to get worse ... so don't buy financials when this data is at its peak (in other words do not buy).

(e) DFS earnings are artificially inflated with recoveries and hence earnings will fall when recoveries normalize (in other words do not buy).

(f) The revenue line for all American financials is toast as per the Japanese experience. So far one of the biggest problems for American financials has been falling revenue but that is not widely commented on outside specialist bank analysts. (In other words sell.)

I left it vague because I wanted to encourage comment. I learn a lot from the comment - but I got many emails that thought I was being unfair and simplistic. So I needed to clarify.

Let me tell a story though.

When I first went to visit BofA in Charlotte (and this dates me) I wanted to ask them about credit. They told me they had 36 billion in revenue and 18 billion in costs and 2 billion in credit costs and that I should watch where the revenue and cost lines were going because they drove it.

That turned out to be wrong of course.

But it may not be wrong in the future.

Post Script 2

I think I should say this is not Discover specific. Consumer credit looks about as good (ie safe) an asset as it has ever been. (It can get worse..) It can also be spurious (extend and pretend for instance).

The best comment yet received by email suggests that I should measure the delinquency against availability of cheap rollover credit cards. Why default - or so the argument goes - when someone will give you a balance transfer and extended credit at 2 percent?